How to Build Credit Score Fast: A Step-by-Step Guide

Did you know that over 30% of Americans have a credit score below 650? If you’re trying to build or rebuild your credit score, you’re not alone. Whether you’re starting from scratch or recovering from financial setbacks, building a strong credit score is crucial for qualifying for loans, credit cards, and even renting an apartment.

In this comprehensive guide, we’ll walk you through how to build credit score effectively — with expert tips, actionable steps, and common mistakes to avoid. By the end of this article, you’ll have a clear roadmap to boost your credit score and maintain it long-term.

The Importance of a Good Credit Score

Your credit score plays a major role in your financial life. It’s used by lenders, landlords, and even employers to assess your reliability and financial responsibility. Here’s why building good credit matters:

- Better loan terms: Higher scores mean lower interest rates.

- Approval for credit cards: Many premium cards require good or excellent credit.

- Rentals and utilities: Landlords may check your score before approving a lease.

- Job applications: Some employers review credit reports for certain roles.

Understanding How Credit Scores Work

Credit scores typically range from 300 to 850, with higher scores indicating better creditworthiness. There are two main scoring models:

- FICO Score – Used by most lenders.

- VantageScore – Commonly used by free credit monitoring services.

What Goes Into Your Credit Score?

Both FICO and VantageScore consider several factors when calculating your score:

- Payment History (35%) – Paying bills on time is the most important factor.

- Credit Utilization (30%) – Keeping balances low relative to your credit limit helps.

- Credit Age (15%) – A longer credit history improves your score.

- Credit Mix (10%) – Having a mix of credit types (e.g., credit cards, loans) shows responsibility.

- New Credit (10%) – Opening too many accounts at once can hurt your score.

Step-by-Step Guide to Build Credit Score

If you’re wondering how to build credit score from zero or improve a poor one, here are proven strategies:

1. Check Your Credit Report Regularly

You’re entitled to a free credit report every year from each of the three major bureaus: Equifax, Experian, and TransUnion. Reviewing your report helps you spot errors or fraudulent activity.

Use AnnualCreditReport.com to access your free report annually.

2. Pay Bills on Time

This is the single most impactful way to build credit. Late payments can stay on your report for up to seven years.

- Set up automatic payments

- Use payment reminders

- Pay early if possible

3. Keep Credit Utilization Low

Credit utilization is the percentage of your available credit that you’re using. Aim to keep it under 30%, ideally under 10%.

For example, if your card has a $1,000 limit, try to carry a balance under $300.

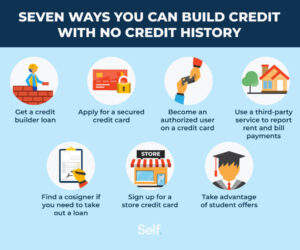

4. Consider a Secured Credit Card

A secured credit card requires a deposit, which acts as your credit line. These cards are ideal for people with no or bad credit.

- Choose a card that reports to all three credit bureaus

- Use it responsibly like a regular card

- Eventually upgrade to an unsecured card

5. Become an Authorized User

If someone in your family has good credit, ask them to add you as an authorized user on their card. Their positive payment history will reflect on your credit report.

Make sure the issuer reports authorized users to the credit bureaus.

6. Use a Credit Builder Loan

These small loans are offered by credit unions and online lenders. You make monthly payments, and once paid off, you get the money back.

It’s a safe way to build credit without risk of debt accumulation.

Best Practices to Maintain a Healthy Credit Score

Once you’ve built your credit, maintaining it is just as important. Here are some best practices:

- Don’t close old accounts: Length of credit history matters.

- Limit hard inquiries: Too many can lower your score temporarily.

- Monitor your credit regularly: Catch issues early.

- Keep balances low: Especially on revolving accounts like credit cards.

- Stay diversified: Mix installment loans and revolving credit.

Common Mistakes That Hurt Your Credit Score

Avoid these common pitfalls to protect your progress:

- Making late payments

- Maxing out credit cards

- Opening too many new accounts

- Closing old credit accounts

- Ignoring errors on your credit report

Expert Tips and Real-Life Success Stories

We spoke with financial advisor Jessica Lee, who shared her insights:

“Building credit isn’t about quick fixes. It’s about consistency. I’ve seen clients go from a 550 to a 720 score in just 18 months by sticking to simple habits like paying on time and keeping balances low.”

Case Study: From No Credit to 700+ in 1 Year

Background: Maria, age 22, had no credit history after college. She started with a secured credit card and made consistent payments.

Strategy: Used the card for small purchases, paid off the balance monthly, and set up automatic payments.

Result: After one year, Maria had a 703 credit score and qualified for a travel rewards card.

Frequently Asked Questions

How fast can I build my credit score?

With consistent on-time payments and responsible usage, you can start seeing improvements in 3–6 months. Significant increases usually take 6–12 months.

Can I build credit without a credit card?

Yes! You can use alternative methods like credit builder loans, becoming an authorized user, or having rent payments reported to credit bureaus.

Does checking my credit hurt my score?

No, checking your own credit report or score is a soft inquiry and does not impact your credit score.

What is a good credit score?

A score above 670 is considered good. Anything above 740 is excellent and opens doors to the best credit offers.

Will paying off collections improve my credit score?

Paying off collections doesn’t remove them from your report, but it can improve your chances of getting approved for credit and may slightly raise your score.

Final Thoughts

Learning how to build credit score is a powerful step toward financial freedom. Whether you’re starting from scratch or rebuilding, the key is consistency, awareness, and smart financial habits.

If you found this guide helpful, feel free to share it with others who might benefit. Got questions or want to share your credit-building journey? Leave a comment below!

Want to learn more about managing debt while building credit? Check out our guide on Debt Management Strategies.

Also read: Best Credit Cards for Building Credit.

Need help choosing a credit monitoring service? We’ve reviewed the top options in our Credit Monitoring Services Review.

For more information on credit reporting, visit the official Consumer Financial Protection Bureau (CFPB) website.

Check out the Experian site for free credit education tools.